What Is a Protective Put and Who Should Actually Use One?

Trent Pearce

Trent Pearce

A note before we begin: At Rule One Investing, we almost always talk about being the insurance company when it comes to options. This means selling puts, not buying them. The Rule One Put (selling a put to get paid to buy a wonderful company at an on-sale price) is our default options strategy. Protective puts, where you buy a put to protect shares you already own, are a Wall Street standard, but we use them only in specific, limited situations. This article will teach you how protective puts work, explain the Wall Street logic behind them clearly, and then tell you honestly when they do and do not fit the Rule One way of thinking.

Most of the time when I talk about options, I’m talking about being the insurance company.

At Rule One, we usually sell puts. We don’t buy them. There’s a specific reason for that, and I want to make sure you understand the philosophy before we get into the mechanics of protective puts.

When we sell a put, we’ve already done our homework. We’ve identified a wonderful business, run our numbers, and determined that the stock is trading below what we believe it’s actually worth. We want to own it. We get paid a premium to obligate ourselves to buy it at our on-sale price. If the stock drops to our strike price, we get the shares we already wanted. If it doesn’t, we keep the premium and make a solid rate of return while we wait.

That’s the Rule One way. Win-win, either way.

But every insurance contract has two sides. Someone is selling the policy - and someone is buying it. Wall Street investors buy protective puts every day. If you own shares, understanding what a protective put is, how it works, and when it might actually make sense for a Rule One investor is part of understanding the full picture.

So let’s cover it completely.

What is a Protective Put? Why Wall Street Uses One

The Wall Street Definition

A protective put is a two-part position: you own shares in a company, and you buy a put option on those same shares.

That put gives you the right to sell your shares at an agreed-upon price, the strike price, before the option expires. No matter how far the stock falls between now and expiration, your loss is capped. That floor is what you’re paying for. The premium is the cost of it.

Wall Street calls this strategy “protective” because it protects an existing position from catastrophic downside. You already own the shares. You’re uncertain about what’s coming. You pay for a safety net.

Why Wall Street Buys Protective Puts

The Wall Street investor using a protective put is operating from a specific mindset: I own this stock, I’m not certain what’s going to happen, and I want to limit how wrong I can be.

That uncertainty is baked into the strategy. The investor may not have done deep research into the underlying business. They may be holding through an earnings event, a rate decision, or a market downturn they can’t predict. A protective put is their hedge.

And that’s exactly the difference between Wall Street’s use of protective puts and ours.

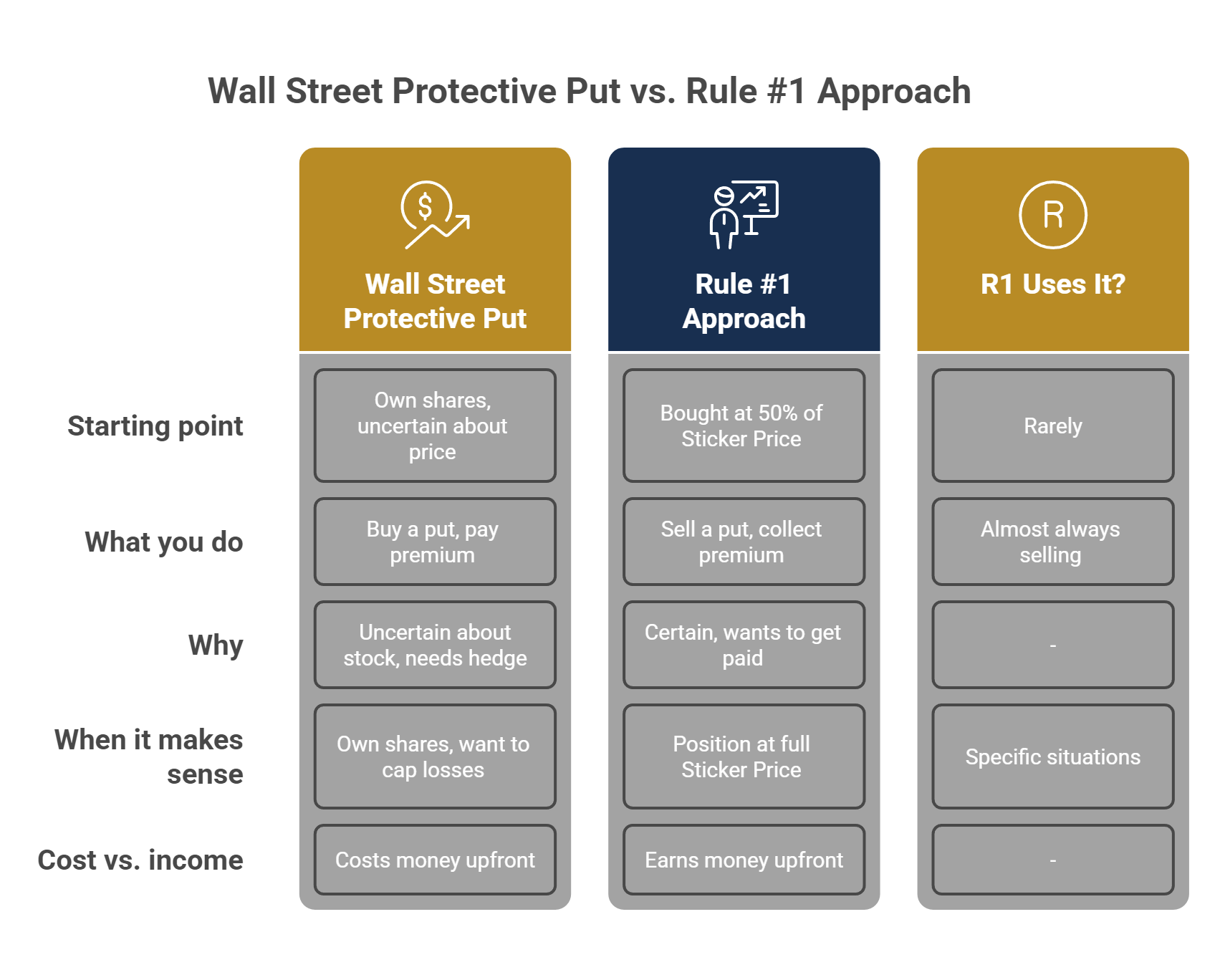

At Rule One, we don’t buy protective puts because we’re uncertain. We only own shares in businesses we’ve researched thoroughly through the Four M’s - Meaning, Moat, Management, and Margin of Safety. We bought at 50% of Sticker Price. That discount is already our cushion. Uncertainty isn’t the problem we’re solving.

How a Protective Put Actually Works

The Mechanics

You own 100 shares of a company. The stock is trading at $100 per share. You buy one put contract covering those 100 shares, with a strike price of $95. The premium costs $3 per share. Total out of pocket: $300.

That $300 is your insurance premium. Here’s what it buys you.

If the Stock Drops

The market gets ugly. The stock falls to $70 per share.

Without the put, you’re down $30 per share. With the put, your floor is $95. Your maximum loss is $8 per share - $5 from the gap between your purchase price and the strike, plus the $3 premium you paid. On 100 shares, that’s $800 total, no matter how far the stock falls below $95.

At that point you have two choices. You can exercise the put and sell your shares at the strike price. Or you can sell the put contract itself on the open market, capture its value, and hold onto your shares.

Important: the loss is only fully capped if you exercise the put contract. If you sell the put for a profit but keep the shares, those shares can continue to fall. Your protection from that point on is only what you realized from selling the put contract.

If the Stock Climbs

The stock climbs to $130. The put expires worthless. You didn’t need it.

You keep the full gain on your shares, minus the $300 premium you paid. Your upside is not capped. The premium reduces your net return but does not limit how high your gains can go.

That $300 is gone either way. That’s the honest trade-off. If the stock falls, it saved you thousands. If the stock rises, it cost you $300 for peace of mind. For most Rule One investors, in most situations, that cost is unnecessary - because the Margin of Safety already provides the cushion.

Rule One vs. Wall Street: The Put Picture Side by Side

This table summarizes how protective puts fit (or don’t fit) into the Rule One framework versus the Wall Street default:

The bottom line: Wall Street buys protective puts out of uncertainty. Rule One investors, when they use them at all, do so out of a very specific kind of certainty. Certainty that a position has grown to full value and they want to protect what they’ve built.

Protective Put vs. Stop-Loss: Why It Matters If You Love the Company

A stop-loss and a protective put both limit how much you can lose on a position. That’s the only thing they have in common.

A stop-loss sells your shares the moment the stock hits a price you set in advance. When it triggers, you’re out. No decision required. It cannot tell the difference between a permanent problem and a temporary one. The stock hits your threshold and the order fires–whether something has fundamentally broken in the business, or whether the market is just having a bad week.

A protective put gives you the right to sell at your strike price. It never forces you to. You stay in control.

For a Rule One investor who has done the Four M’s work, that distinction matters. You bought because you understand the business. A short-term price drop is not automatically a reason to exit. If you look at the drop and decide something has fundamentally changed in the business, you exit. If you look at it and decide nothing has changed–the moat is intact, the management is sound, the price dropped because Mr. Market got emotional–you hold. Or better yet, you buy more.

Stop-losses can also trigger on intraday volatility, a sudden dip that recovers by the end of the same day, and leave you watching the stock climb back without you. A protective put does not work that way. It holds its floor regardless of intraday noise.

If you own a position you love and want to stay invested through a rough stretch without being forced out, a protective put preserves your decision-making power. A stop-loss takes it away.

When a Protective Put Actually Makes Sense for a Rule One Investor

It Starts with the Margin of Safety

When you buy a wonderful company at 50% of its Sticker Price, you already have significant downside protection built in. That 50% discount is your cushion. The Margin of Safety is the first line of defense. In most situations, especially early in a holding, you don’t need a protective put on top of it.

If the stock drops while you’re holding at 50% of Sticker Price, the Rule One response is not to buy a protective put. It’s to buy more shares, if the business story hasn’t changed. The price drop is Mr. Market being emotional. We take advantage of that, we don’t hedge against it.

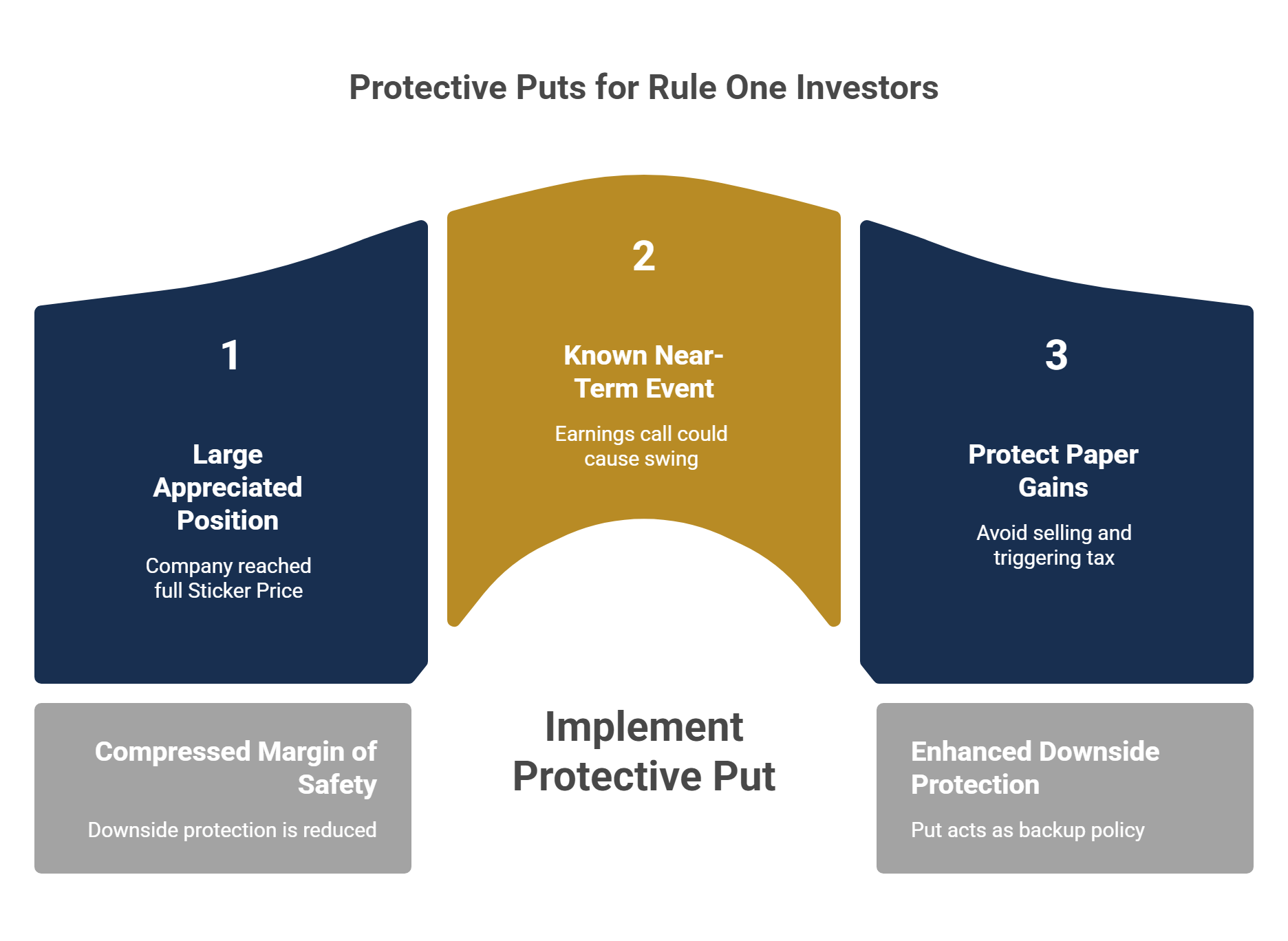

When the Calculus Changes

The situation shifts when your position has appreciated significantly.

You bought at a deep discount. The stock has run up toward or beyond its Sticker Price. That is exactly what Rule One is designed to produce. But as the stock climbs, your original Margin of Safety compresses. The 50% discount that protected you on the way in is no longer your cushion.

That is the moment a protective put becomes worth considering. Specifically:

The company has run to full Sticker Price value, and you’re holding a large, appreciated position.

A known, near-term event, like an earnings call, could create a significant price swing in either direction.

You want to protect substantial paper gains without selling and triggering a tax event (worth discussing with a tax professional before acting).

In those situations, a protective put steps in where the Margin of Safety left off. The built-in buffer that served you on the way in can no longer carry the full weight of your downside protection. The put becomes the backup policy.

Example: You bought a wonderful company at $50 when the Sticker Price was $100. The stock has now run to $200 - well above Sticker. An earnings call is coming up in three weeks that could move the stock significantly in either direction. You don’t want to sell (you’d trigger a major tax event), but you want to protect what you’ve built. Buying a put at or near your exit price gives you that protection for the duration of the event. That is the Rule One use case for a protective put.

So Who Should Actually Use One?

It Makes Sense If You’re in One of These Situations

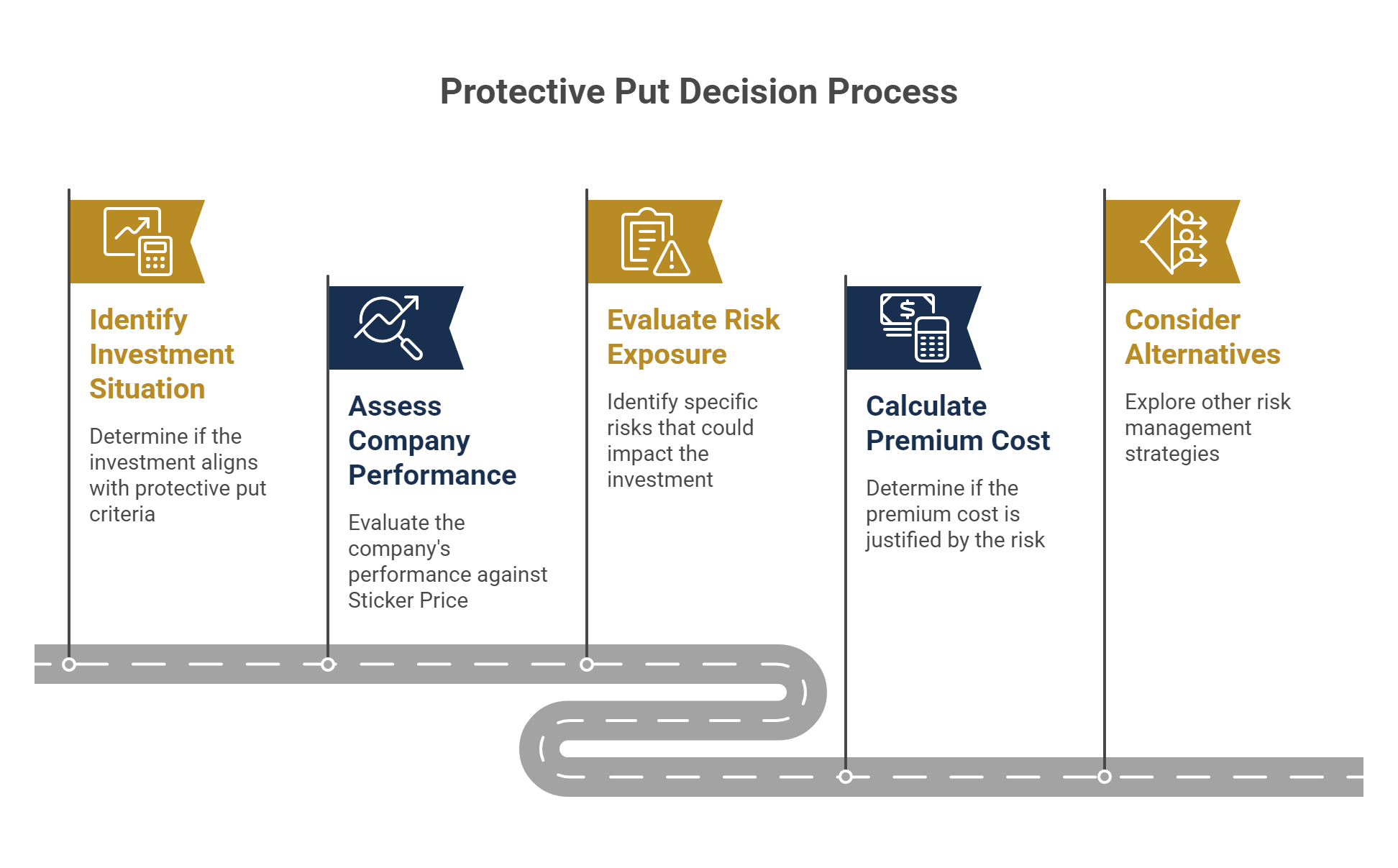

A protective put is not for every investor. It is a specific tool for specific circumstances.

You’ve done the Four M’s work and own a wonderful company

AND

that position has run to or beyond its Sticker Price.

You’re sitting on significant gains you want to protect without selling - and a near-term event creates meaningful risk to that position.

The premium cost is justified by the specific risk you’re protecting against, not just general market anxiety.

When a Protective Put Is Probably Not the Right Tool

Most options content skips this part. We won’t.

You bought at 50% of Sticker and the stock has dipped. You don’t need a put, you need conviction. The Margin of Safety is doing its job. In most cases, a drop means an opportunity to buy more, not a reason to buy insurance.

You haven’t done the research. If you’re not sure whether the business is wonderful, the problem isn’t the lack of a protective put. The problem is the position itself. A put doesn’t fix uncertainty about the underlying business. It just makes that uncertainty more expensive.

You don’t own the underlying shares. Without stock ownership, you’re not hedging. You’re buying a speculative put, a bet the stock will fall. That’s not what we teach, and it’s not what this article is about.

The cost feels too high. Protective puts are not cheap, especially on volatile stocks. If the premium is significant relative to the protection you’re getting, there may be better tools for your situation.

What Does Protection Actually Cost?

The Premium Is Real Money and It’s Gone Either Way

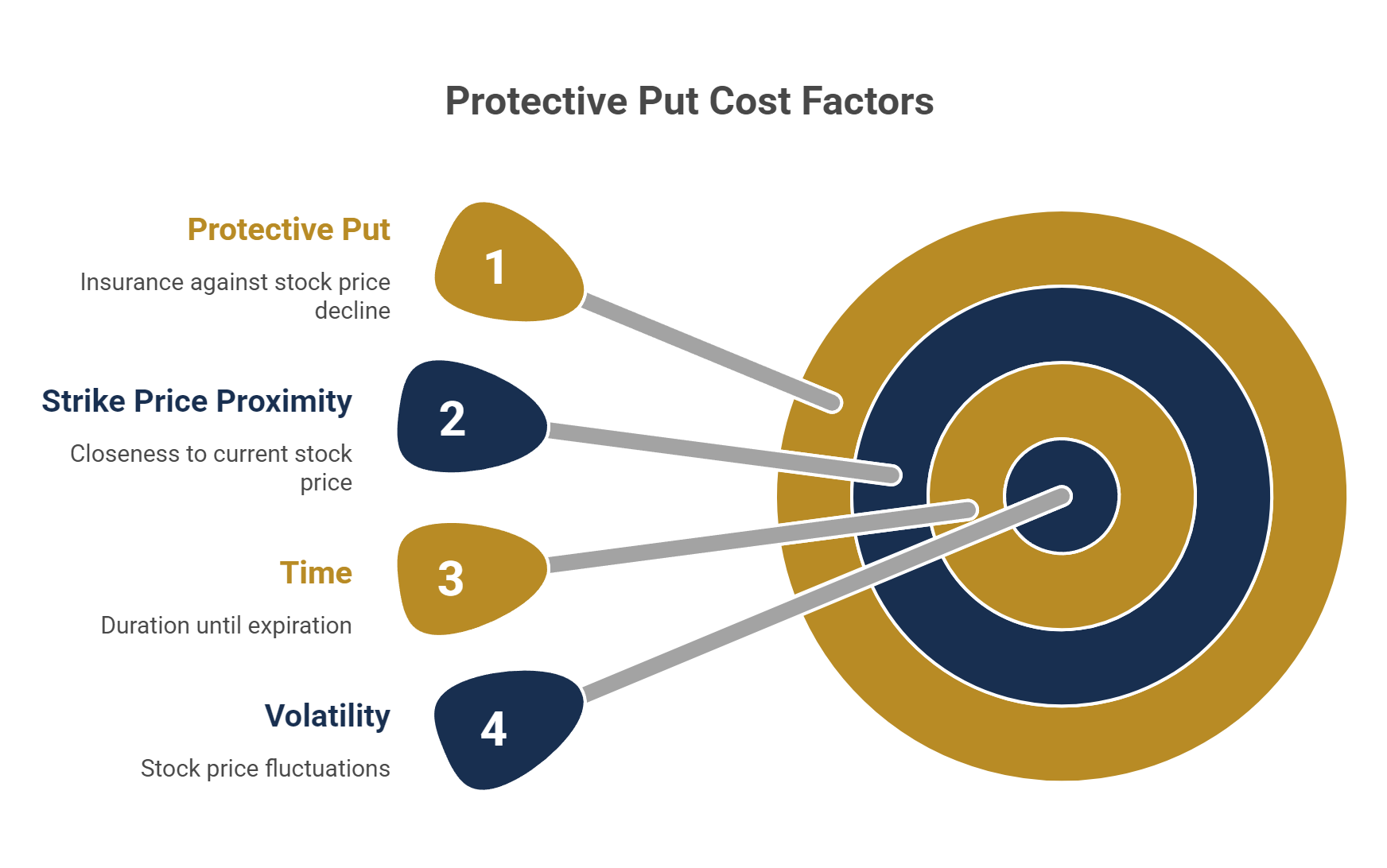

The premium you pay is a real, non-recoverable expense. If the stock climbs and the put expires worthless, that money is gone. What you’re actually buying is not a payout. It’s certainty. You know your worst-case number before it happens. For the right investor in the right situation, that is worth paying for.

Three Things Determine What You Pay

Strike price proximity. The closer your strike is to the current stock price, the more the put costs - but the more protection you get from day one. A lower strike is cheaper but leaves a bigger gap before your floor kicks in.

Time. The further out the expiration date, the more the put costs. The put will also gradually lose value as expiration approaches.

Volatility. Puts on stocks that move around a lot cost more than puts on stable ones. More volatility means a higher probability the put gets used, and that gets priced in.

Buying a Put and a Protective Put Are Not the Same Thing

Buying a put without owning the underlying shares is a speculative bet that the stock will fall. That is not what we teach, and it is not what this article is about.

A protective put only exists in combination with a stock position you already own and intend to keep. That pairing is what makes it a hedge. Remove the stock ownership and the word “protective” no longer applies.

Rule One investors use options to generate income on businesses they want to own, or to protect positions in businesses they believe in. Not to bet against companies. That distinction matters.

Ready to See the Full Picture?

Most investors only ever learn one side of the options contract. Now you know both.

At Rule One, we spend most of our time on the sell side - generating income through strategies like Rule One Puts and bull put spreads while we wait for wonderful companies at the right price. The protective put completes that picture. You understand what you’re selling. You understand what the person on the other side is paying for, and why.

If you want to see how the full options picture fits together - when to sell, when to protect, and how to build a disciplined strategy around businesses you actually believe in - join us at the Rule One Virtual Investing Workshop. That’s where this conversation goes deeper.

One weekend. The full picture.

Phil Town

Phil Town is an investment advisor, hedge fund manager, 3x NY Times Best-Selling Author, ex-Grand Canyon river guide, and former Lieutenant in the US Army Special Forces.