Vertical Spreads Explained: How to Generate Cash Flow While You Wait for the Right Investment

Trent Pearce

Trent Pearce

If you've been building your Rule One foundation for a while, you've probably come across options at some point and wondered whether they fit into this approach. Maybe you heard the term vertical spread, went looking for a clear explanation, and found something that felt like it was written in a foreign language.

That's not a coincidence. Wall Street doesn't make this stuff for the average person to understand, and part of that, in my opinion, is intentional. The more complicated it seems, the more dependent you feel on the professionals. That dependence is very good for them.

Here's what I want you to know: the logic behind these strategies is something you already understand from everyday life. Think about how a car insurance company operates. It gets paid upfront, takes on a defined obligation, and structures everything so the odds are in its favor.

Once you see credit spreads through that lens, and it's a lens I've used since teaching options and risk management in the Rule One advanced programs, the confusion starts to clear up pretty quickly.

One important note before we go further: everything I'm going to walk you through should be practiced in a simulated paper trading account before you put real money on the line. Paper trading lets you learn the mechanics, test your decision-making, and build confidence, all without any real capital at risk.

At Rule One, our students work through these strategies in a simulated environment first. That's not optional. It's how you build the foundation to do this well.

First, Why Would a Rule One Investor Use Options at All?

The Waiting Problem

Rule One Investing has a clear process. You find a wonderful company, one you understand deeply, with a durable competitive advantage, trustworthy management, and a real Margin of Safety in the price. Then you wait for Mr. Market to put it on sale. When he does, you buy it and hold it.

That process works. But it comes with a natural friction: the waiting. Sometimes the company you've researched isn't on sale yet. The price is too high. You're staying patient and disciplined, doing exactly what a Rule One investor should do. In the meantime, your capital is sitting there doing very little for you.

A Cash Flow Tool for the Time in Between

Credit spreads are a way to put that capital to work while you wait. You generate income by operating on the right side of probability, collecting premiums rather than letting your money sit idle between investments.

This Is Trading, Not Investing

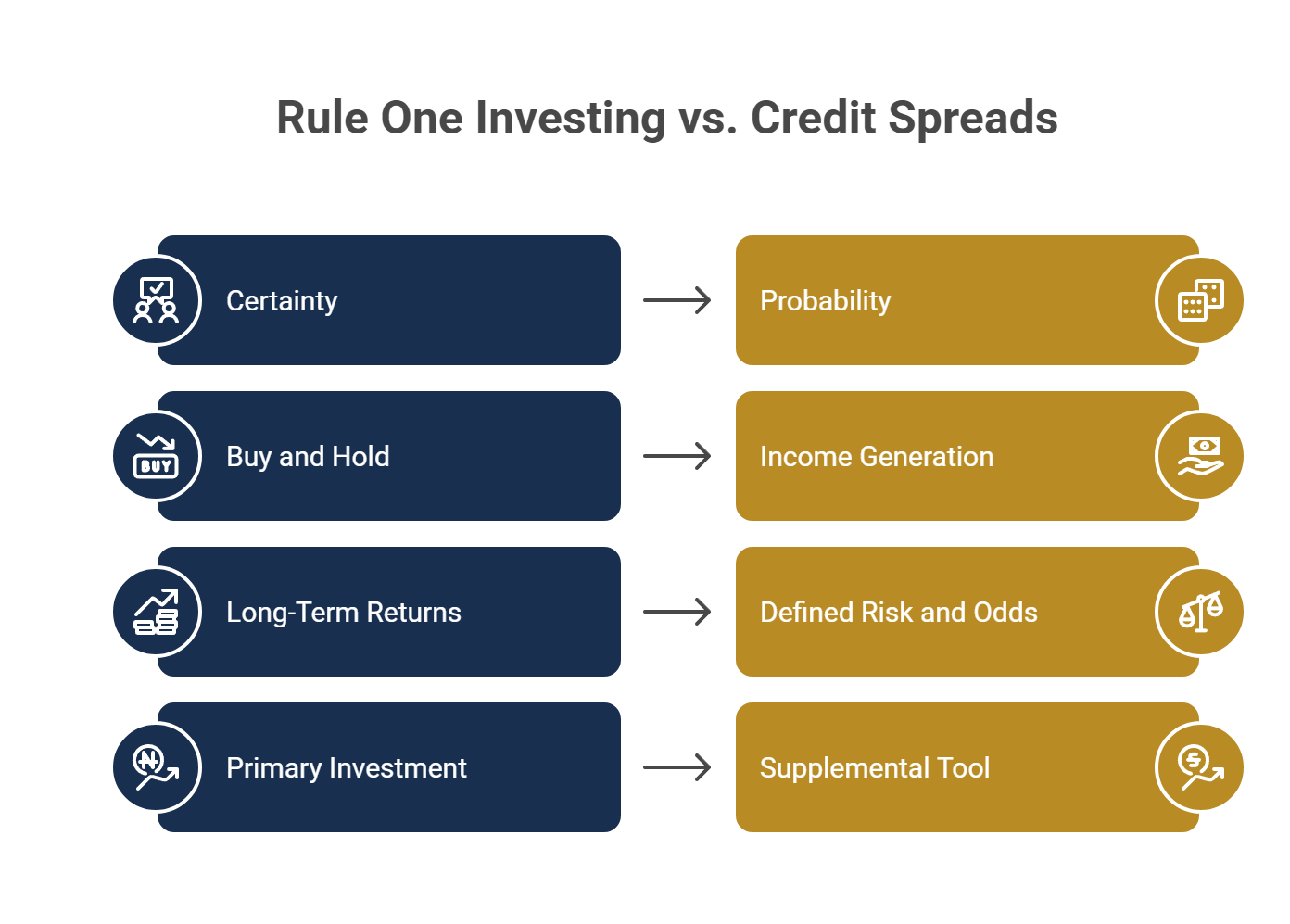

I want to be straight with you about something, because I think it matters. This is not Rule One Investing. Rule One Investing is about acting with certainty. You've done the research. You know the business. You're buying because the numbers and the story both give you conviction. That's what we teach in the core Rule One curriculum, and it's where the best long-term returns come from.

Trading credit spreads is a different activity entirely. You're working with probability, not certainty. And when you trade on probability, losing trades are part of the model. That's not a flaw. It's expected and accounted for. The goal is to structure each trade so your maximum loss is defined upfront and your odds of winning are in your favor, not to win every single time.

Credit spreads don't replace Rule One investing. The best long-term returns still come from buying wonderful businesses at attractive prices and holding them. These strategies are a cash flow tool for the time in between. Both have a role, and it's important to keep them clearly separate in your mind.

So What Exactly Is a Vertical Spread?

The Basic Structure

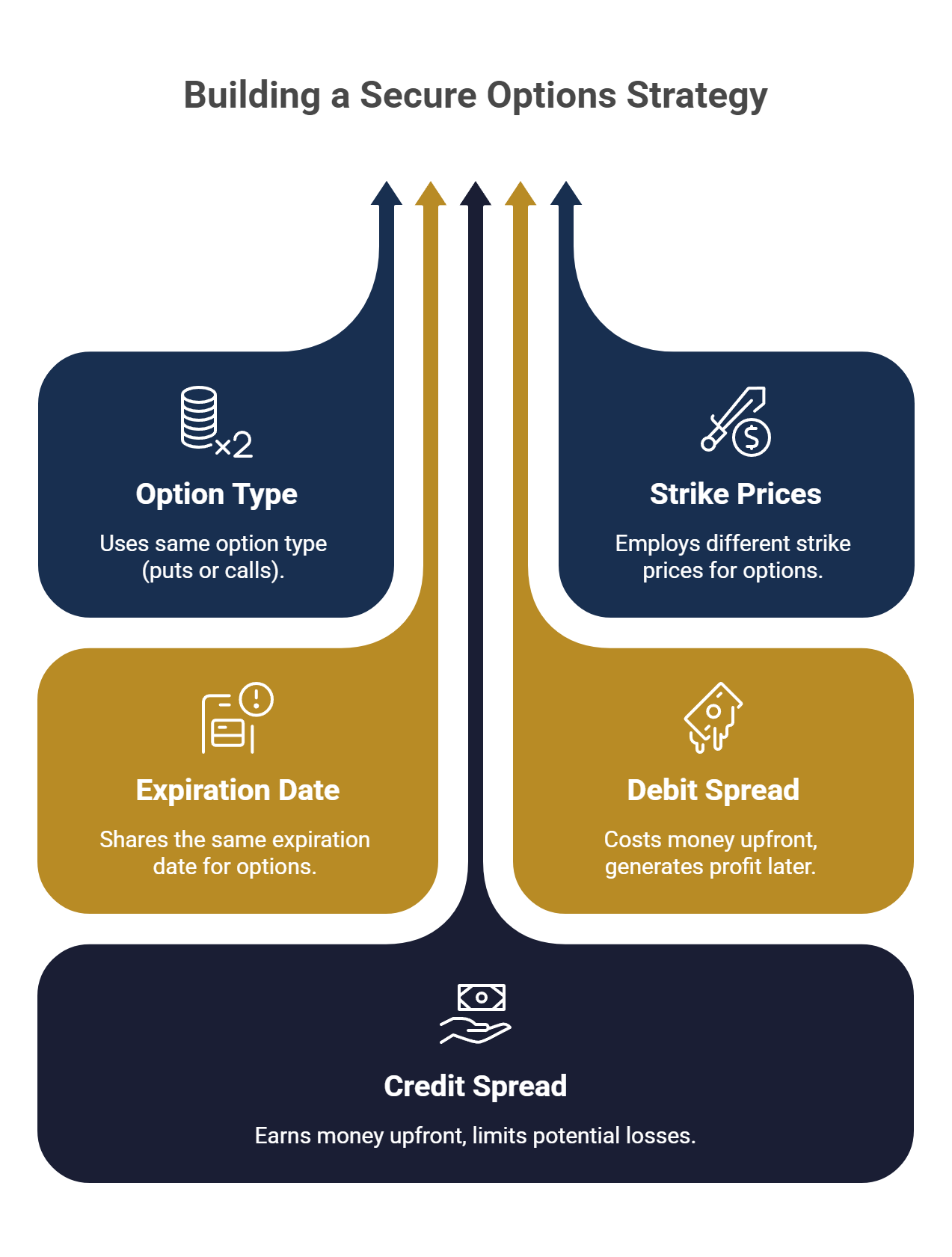

A vertical spread is an options trade made up of two options of the same type, either both puts or both calls, on the same underlying stock, with the same expiration date, but at two different strike prices. You buy one and sell the other at the same time.

The word "vertical" simply refers to how those two strike prices appear on an options chain. One sits above the other. That stacking is what gives the strategy its name.

Debit vs. Credit: What's the Difference?

There are two ways a vertical spread can be set up, and which one you use determines whether you pay to enter the trade or get paid to enter it.

A debit spread costs you money upfront. You pay a net premium to open the position. A credit spread works the other way: you collect a net premium when you open it. That credit hits your account when the trade fills.

This article focuses entirely on credit spreads. Debit spreads have their place, but for a Rule One investor looking to generate cash flow between investments, credit spreads are the relevant tool.

Where the Insurance Company Comes In

Remember the analogy from the introduction. An insurance company collects a premium upfront, takes on a defined obligation if something goes wrong, and structures everything so the odds are working in its favor over time.

That's exactly what a credit spread does. When you sell a credit spread, you step into the role of the insurance company. The premium you collect when you open the trade is your maximum profit. The structure of the spread, specifically the second option you buy as part of the position, caps your maximum loss. You know both numbers before you place the trade.

That defined risk is the foundation of why this strategy fits inside a Rule One mindset. Rule One starts with one principle: don't lose money. A credit spread builds that discipline directly into the structure of the trade itself.

The Insurance Company Analogy (This Is the Key)

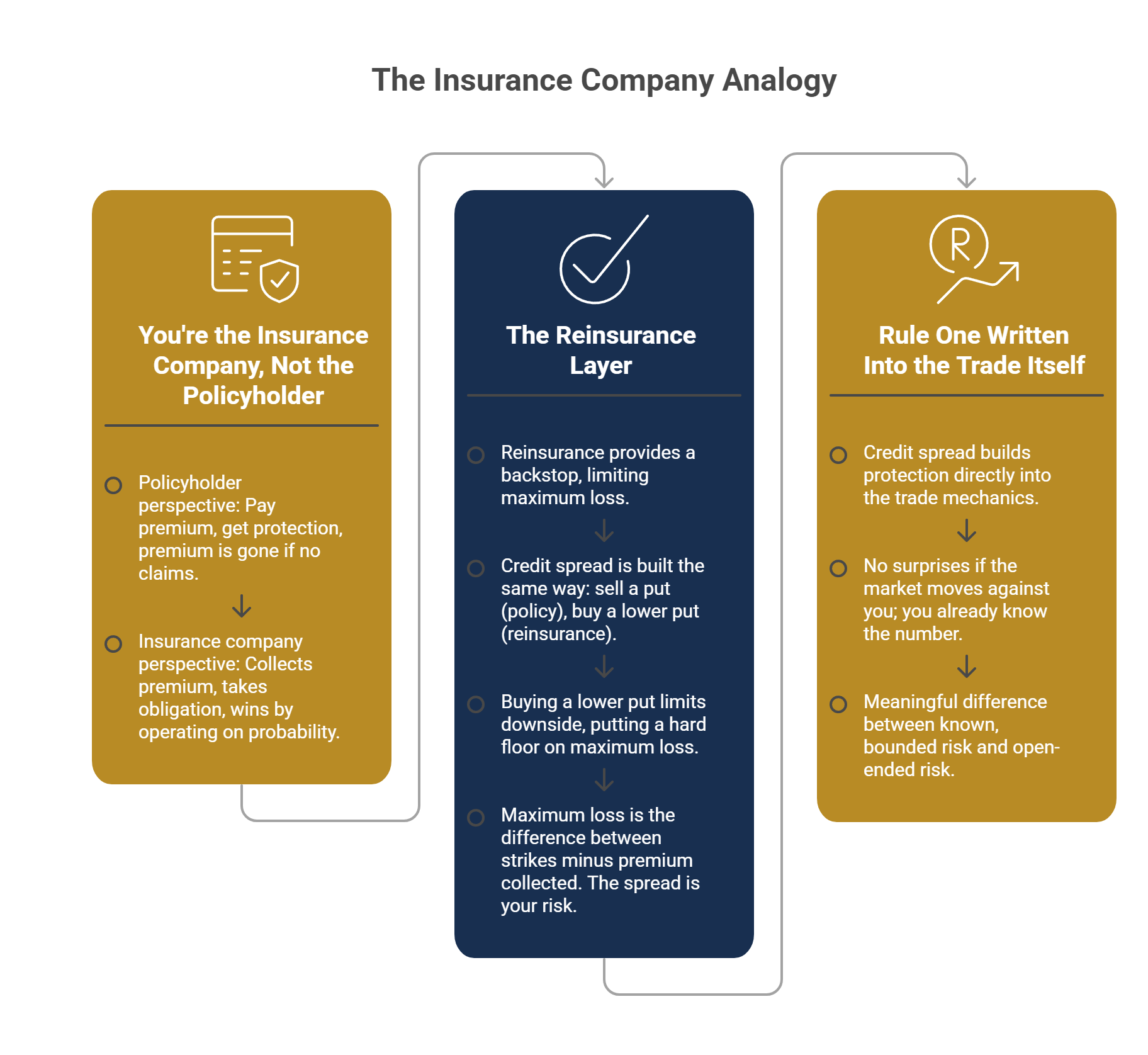

You're the Insurance Company, Not the Policyholder

Here's the question I want you to sit with for a moment: when you think about car insurance, which side of that relationship are you on?

Most of us are on the policyholder side. We pay a monthly premium. If something goes wrong, the insurance company steps in. If nothing goes wrong, that premium is gone. We got nothing back for it. That's just the cost of protection.

The insurance company is in a completely different position. It collects the premium. It takes on the obligation. And because it prices things carefully, it collects more in premiums over time than it ever pays out in claims. It wins by operating on the right side of probability. That's the whole business model.

When you sell a credit spread, you step into that role. You're the insurance company, not the policyholder.

The Reinsurance Layer

Now here's where it gets interesting. Large insurance companies don't just write policies and hope for the best. They protect themselves by buying their own insurance, something the industry calls reinsurance. They cover individual claims on their own, but if a catastrophic event comes through and wipes out everything at once, they've got a backstop that limits how much they can lose. They know their worst-case scenario going in.

A credit spread is built exactly the same way.

When you sell a put option, you collect a premium and take on an obligation to buy shares if the stock falls to your chosen strike price. That's your first policy. But selling that put on its own leaves you exposed to substantial, open-ended downside if the stock keeps falling well below that strike. That's a risk that doesn't sit well with a Rule #1 investor.

So you buy a second put option at a lower strike price. That's your reinsurance. It costs a portion of the premium you just collected, and in exchange, it puts a hard floor under your maximum loss. No matter how far the stock falls, your loss cannot go beyond the difference between the two strike prices, minus the premium you collected. The gap between those two strikes is the spread. The spread is your risk. You know exactly what it is before you place a single dollar.

Rule One Written Into the Trade Itself

The foundation of Rule One is one principle: don't lose money. It's something I come back to constantly when teaching portfolio management and risk mitigation in the advanced programs, and it applies just as much to how you structure a trade as it does to which businesses you choose to buy.

A credit spread doesn't just protect you in theory. It builds the protection directly into the mechanics of the trade. Your worst-case outcome is defined before you open the position. There are no surprises waiting for you if the market moves against you. You already know the number.

That's not about eliminating risk. These trades carry real risk and I'm not going to pretend otherwise. But there's a meaningful difference between risk that is known, bounded, and accounted for, and risk that is open-ended. A credit spread keeps you on the right side of that line.

The Bull Put Spread: The Primary Credit Spread Strategy

Of the two credit spread strategies I'm going to walk you through, the bull put spread is the one we focus on most in the Rule One advanced programs. It's the workhorse, and it's a strategy we come back to again and again at Rule One. It's especially well suited for those with smaller amounts of capital who are working to build up their investment portfolio. If you understand this one well, the other will make immediate sense because it's essentially the mirror image.

How a Bull Put Spread Works

Here's the basic setup:

You sell a put option below the current stock price, collecting a premium upfront.

At the same time, you buy a second put option at an even lower strike price, paying a smaller premium.

Both options are on the same stock and expire on the same date.

The difference between what you collected and what you paid is your net credit. That credit lands in your account when the trade fills, and it's also your maximum profit. You cannot make more than what you collected upfront.

In terms of outcomes:

If the stock goes up, you win.

If it stays flat, you win.

If it dips only modestly, you win.

You only lose if the stock falls significantly below the strike price you sold.

Think of it like the insurance company again. The insurance company wins when you don't crash the car. The bull put spread wins when the market doesn't crash.

The Numbers in Plain English

Let me walk you through how the key figures work using round numbers. This is a straightforward illustration, not a specific trade recommendation. Actual results will vary.

Say a stock is trading at $100. You sell a put at the $95 strike and collect a $1.50 premium per share. At the same time, you buy a put at the $90 strike and pay $0.50 per share. Your net credit is $1.00 per share, or $100 per contract, since one contract controls 100 shares.

Here's how the math breaks down:

The spread: the difference between the two strike prices. $95 minus $90 equals $5.

Capital required: spread times 100, minus the premium collected upfront. In this illustration: $500 minus $100, so $400 per contract.

Maximum profit: the net credit collected, $100 per contract. You make this if the stock stays above $95 at expiration.

Maximum loss: spread width minus net premium, times 100. Here, $4 times 100, or $400 per contract. You know this number before the trade is placed.

Breakeven: short put strike minus net premium received. $95 minus $1.00 equals $94. Above $94 at expiration, the trade is profitable to some degree.

When Does a Bull Put Spread Make Sense?

This strategy works best when:

You have a moderately bullish or neutral outlook on a stock or index. You don't need the stock to go up significantly. You just need it to not fall significantly.

Implied volatility is elevated. Higher volatility means richer premiums, which means more income when you open the trade.

You can place the trade below meaningful technical support levels. Fibonacci levels are one tool I use to identify floors where a falling stock is more likely to reverse before reaching your short strike. That's a deeper conversation for a dedicated article on technical indicators, but placement matters.

You want defined risk without tying up the capital required to own shares outright.

When to Exit

There are two ways a credit spread trade ends, and it's worth understanding both before you place your first one.

The winning outcome: the stock stays above your short strike, the trade expires out of the money, and you keep the full premium you collected at entry. That's the most common result. You placed the trade at roughly a 90% probability of winning. Most of the time, you simply let it play out.

The loss management exit: if the stock falls and starts moving against you, your probability of winning begins to shrink. You don't wait for a full loss. The rule is straightforward.

Watch your probability out of the money every day. You placed the trade at 90% or higher. If it starts falling, pay attention.

When it drops to 70% or below, close the credit spread trade immediately. On Thinkorswim, that figure is displayed directly on the platform.

If you're on another broker, use the Delta reading instead. A Delta of 0.3 or above is your equivalent signal to exit.

Think of it like the insurance company analogy. The moment you see your policyholder getting on the interstate at 120 miles an hour, you don't wait for the crash. You close out the policy and move on to the next driver. That's exactly what this rule does.

Closing a credit spread can be an emotional experience, and that's exactly why we have rules.

When a trade moves against us, our emotions start whispering, "Just hold on a little longer... it might turn around." That's the moment our rules matter most. They keep us logical when our feelings are pushing us toward hope instead of discipline. Remember: your first loss is your best loss. Taking a small, controlled loss beats riding a bad trade into a much bigger one.

The good news? We expect this. We plan for occasional losses, and that's why we make sure our winning trades generate enough profit to comfortably cover them. Over time, staying disciplined and sticking to the rules is what makes the strategy work.

The Bear Call Spread: The Mirror Image

If you understood the bull put spread, the bear call spread will take about 30 seconds to grasp. It's the same logic, the same structure, and the same defined-risk framework. The only thing that changes is direction.

The Setup

With a bull put spread, you place the trade below the current stock price and win if the market doesn't crash. With a bear call spread, you place the trade above the current stock price and win if the market doesn't spike dramatically higher.

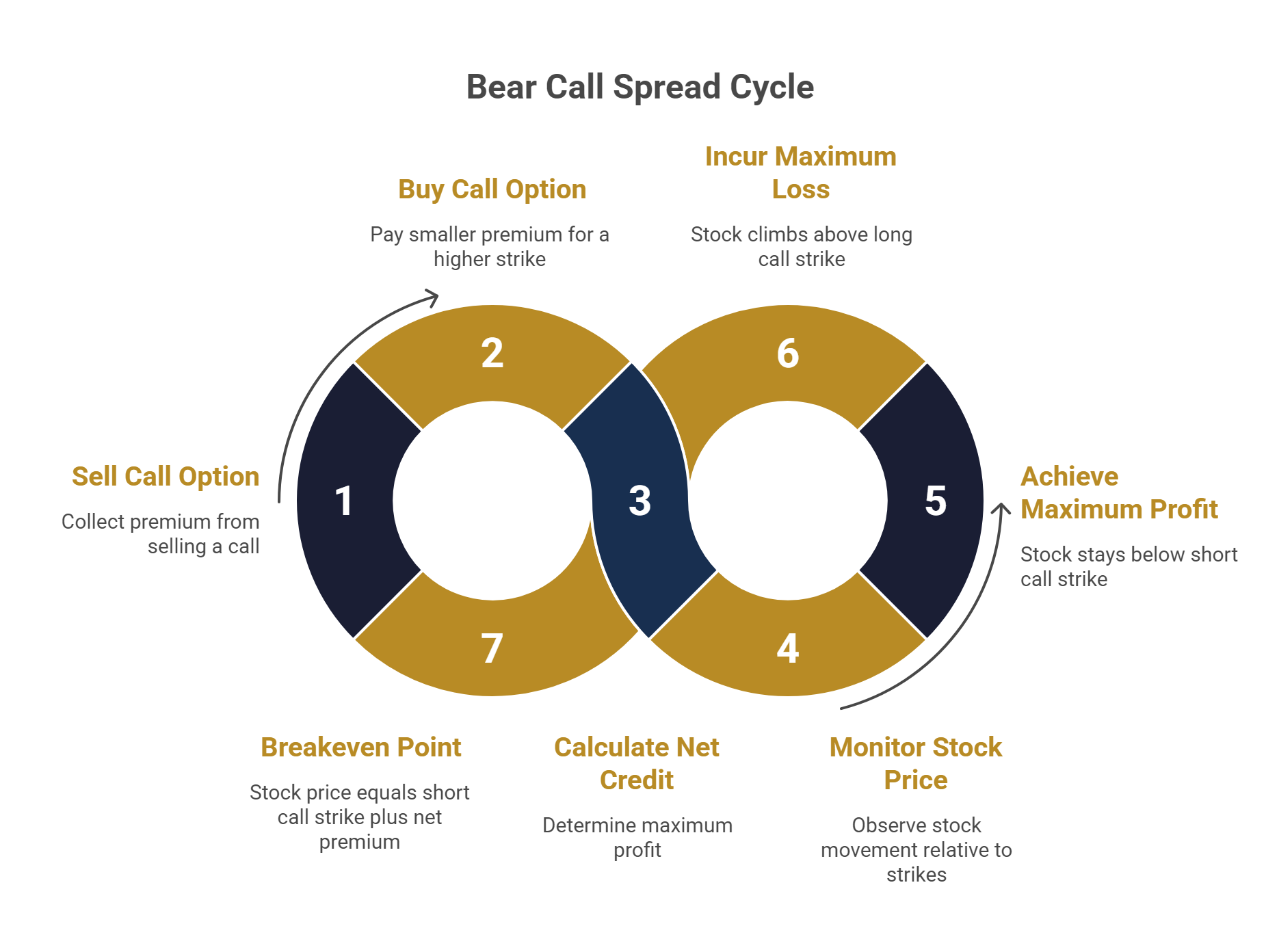

Here's how it works:

You sell a call option above the current stock price, collecting a premium.

At the same time, you buy a second call option at a higher strike, paying a smaller premium.

The difference is your net credit, and that's your maximum profit.

You win if the stock goes down, stays flat, or rises only modestly.

You lose if the stock climbs significantly above the strike price you sold.

The same reinsurance structure applies. The call you buy at the higher strike caps your maximum loss. Your worst-case outcome is defined before you open the position.

An Illustrative Example

Using the same round numbers as before. This is a straightforward illustration, not a trade recommendation. Actual results will vary.

Say a stock is trading at $100. You sell a call at the $105 strike and collect $1.50 per share. You buy a call at the $110 strike and pay $0.50 per share. Your net credit is $1.00 per share, or $100 per contract.

The spread: $110 minus $105 equals $5.

Capital required: $500 minus $100 collected, so $400 per contract.

Maximum profit: $100 per contract, achieved if the stock stays below $105 at expiration.

Maximum loss: $400 per contract, if the stock closes above $110 at expiration.

Breakeven: short call strike plus net premium received. $105 plus $1.00 equals $106.

When to Use It

The bear call spread makes sense when you expect a stock or index to stay range-bound or drift lower, and you want to generate income from that view without owning puts outright. It also tends to be more attractive when call premiums are elevated, giving you more credit to collect upfront.

In my own credit spreads, the bull put spread strategy is the strategy I lean on most. But when conditions favor it, the bear call spread operates on exactly the same probability-based logic. Same insurance company model, same exit discipline, just placed on the other side of the market.

What Vertical Spreads Are Not

One more thing worth saying clearly, now that you understand how these trades work.

The temptation, once the mechanics click, is to start treating credit spreads as a primary strategy rather than a secondary one. Don't do that. The income they can generate is real, but it comes from probability, not from the deep business knowledge that makes Rule One investing work. These are different engines. They're designed for different jobs.

Credit spreads work well when they stay in their lane: generating cash flow while you wait for the right investment. The moment you start substituting them for the harder, slower work of finding and valuing wonderful companies, you've lost the plot.

Use each tool for what it was built to do, and you'll get the best out of both.

Ready to See This in Action?

Understanding the mechanics on a page is the starting point. Placing a real trade, with a coach next to you, is where it actually clicks.

What makes our approach different is that we don't just teach you how to execute a credit spread. We give you a proprietary set of criteria to evaluate the trade before you enter it. These filters help you quickly determine whether a setup meets our standards, so you're not guessing. You know if the trade is worth taking before a single dollar is on the line.

The Rule One Virtual Investing Workshop is where that all comes together. You practice in real time with live Rule One mentors, including instructors from the advanced programs who work with these strategies as full-time investors themselves. Not just watch and listen, you actually do it.

Phil Town

Phil Town is an investment advisor, hedge fund manager, 3x NY Times Best-Selling Author, ex-Grand Canyon river guide, and former Lieutenant in the US Army Special Forces.