Should I Hire a Financial Advisor? Why You Probably Don't Need One

Phil Town

Phil Town

Many people believe that hiring a financial advisor is essential for making good investment decisions. This myth has been reinforced by decades of marketing from many financial advisors, but the truth is, many investors who manage their own money often achieve better results than those who rely on advisors, without fees eating into their returns or jeopardizing their financial future.

If you're wondering, "Do I need a financial advisor to secure my financial future and reach my long term goals?", consider these critical points as you develop your own financial plan.

[r1-johnsonbox name="Best Investors Guide B"]

The Short Answer: Do You Need a Financial Advisor?

Whether you are asking 'do I need a financial planner' or wondering if an advisor is worth the cost, here is the honest answer: for most everyday investors, no.

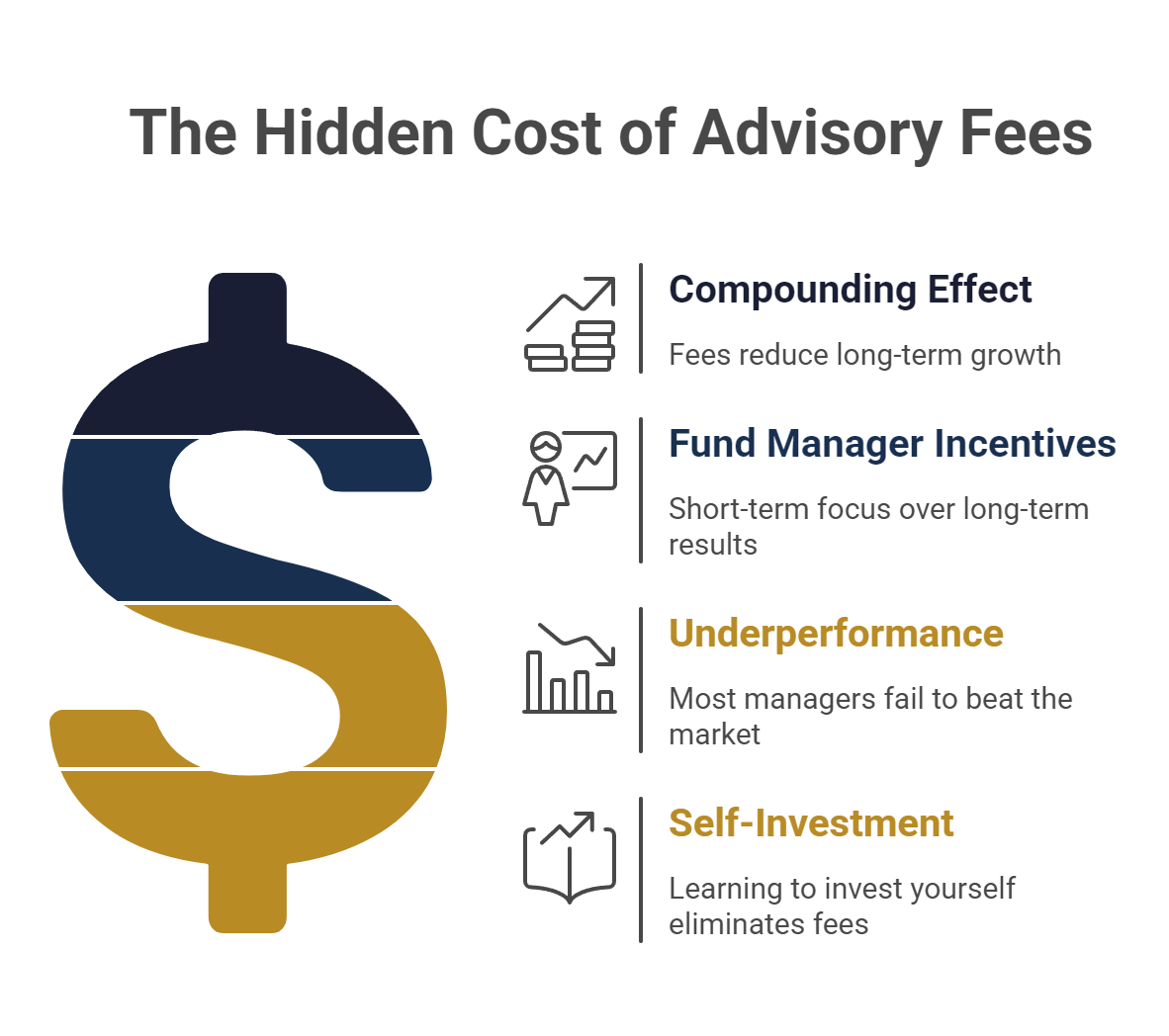

Not because financial advisors are bad at what they do. Many of them genuinely care about their clients. The problem is the system they operate inside, one built around annual fees of 1-2% of your portfolio, charged every year regardless of how your investments actually perform. That fee structure compounds against your wealth the same way good investments compound for you. Over a lifetime, the math is brutal.

The good news is that the specific job most people hire an advisor for, evaluating investments and deciding what to own, is something you can learn to do yourself. The Rule #1 Four Ms framework gives you a structured, repeatable process for doing exactly that. That is what this page is about.

There are real exceptions. Complex estate planning, multi-state trust structures, or business sale tax strategy may call for a fee-only specialist. But investment management itself? That is the part you can take back.

Financial Advisors Don't Try to Beat the Market

A common misconception is that financial advisors are skilled stock pickers who aim to outperform the market. However, beating the market is not a financial advisor's job.

Instead, financial advisors primarily serve as coaches and counselors who:

Help set financial goals and provide personalized guidance.

Keep you from making emotion-based decisions with behavioral coaching.

Guide you through market downturns and uncertainty.

While this hand-holding can be valuable for some clients, you must decide if it's worth paying an annual fee of 1% (or more) of your portfolio for these services.

Why Don't Financial Advisors Beat the Market?

Financial advisors operate under strict regulations that limit them from using many high-performance investment strategies, including advanced portfolio management and asset location techniques. They are encouraged to use ultra-diversified portfolios, which tend to mirror the market's performance rather than exceed it.

Additionally, the Efficient Market Hypothesis (EMH), which suggests that no one can consistently beat the market, underpins the financial industry's core philosophy. Many financial advisors follow this theory and build portfolios that track the market rather than outperform it, regardless of market conditions.

So, if financial advisors aren't designed to beat the market, what exactly are you paying for? Often, it's advice, guidance, and serving as a sounding board for your financial decisions.

[r1-cta-banner name="Transformational Webinar B"]

Financial Advisors Charge You Regardless of Performance

One of the biggest drawbacks of working with a financial advisor is that their cost is based on the size of your assets, not on how well they grow your money or investments.

How Financial Advisor Fees Work

Most financial advisors charge an Assets Under Management (AUM) fee, typically around 1% per year.

That means:

If you invest $100,000, you pay $1,000 per year, even if your portfolio loses money.

If you invest $1 million, you pay $10,000 per year, regardless of past performance.

This system creates a misalignment of incentives. A certified financial planner gets paid whether or not they generate good returns, so their primary goal is to keep your money under their management rather than maximize your wealth.

Are There Performance-Based Financial Advisors?

Some advisors operate on a performance-based fee structure, where they only take a percentage of your profits. However, these types of advisors are rare and usually cater to high-net-worth individuals. If you're looking for a fee only advisor or a certified financial planner, always ask about their fee structure and services.

For most investors, paying a 1% fee every year can severely eat into long-term returns and erode your confidence in your financial plan.

The Real Cost of Advisory Fees Over Time

Here is the math most advisors never walk you through.

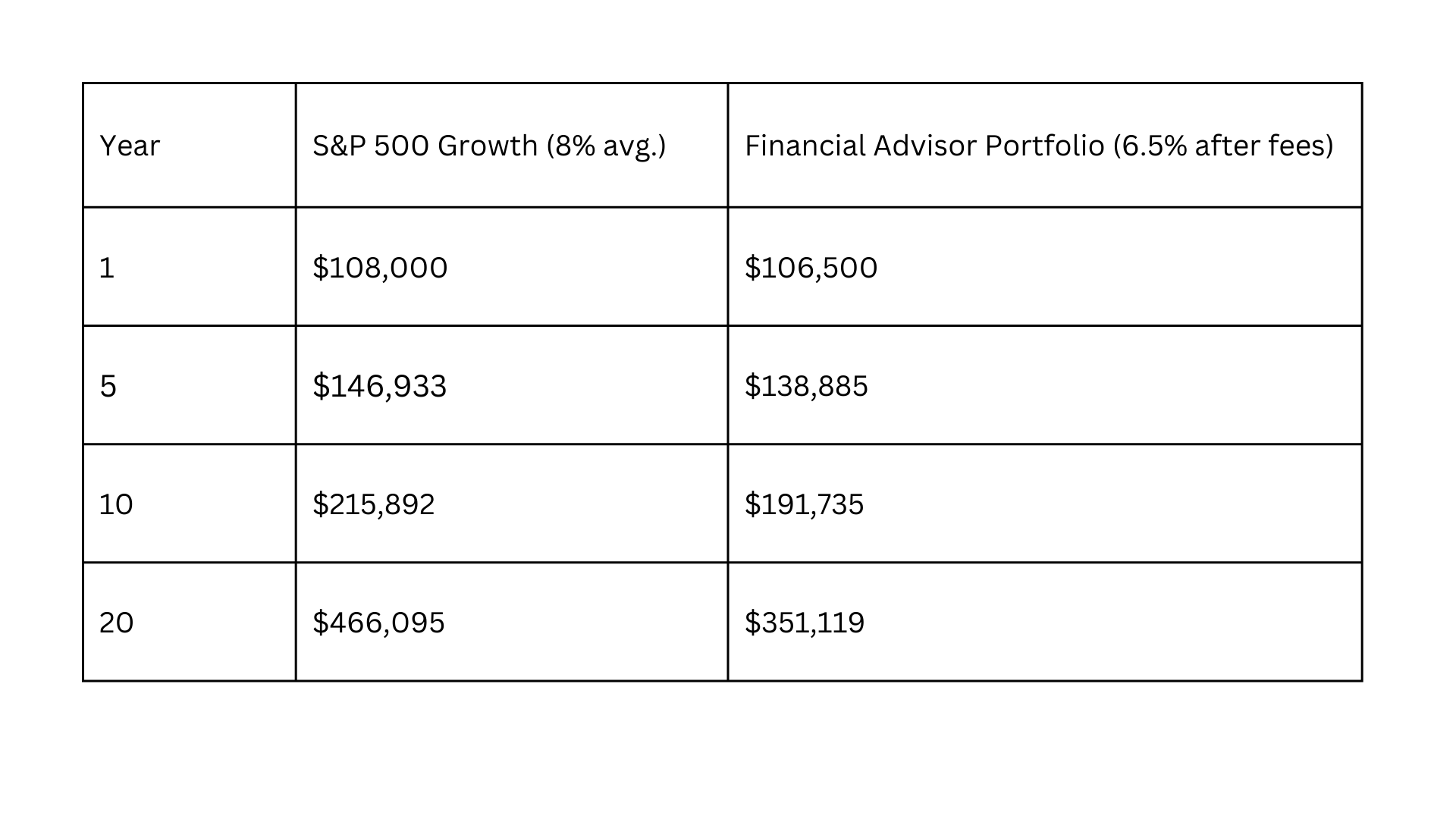

Take a straightforward example. Put $1,000 a month into a 401(k) mutual fund over 20 years. After fees, that fund delivers around 6% annually. The result is roughly $440,000 after two decades of disciplined saving. Invest that $440,000 at retirement and you are generating about $21,000 a year to live on.

That is not a retirement. That is a problem.

And here is the part worth understanding clearly: the fee is not just a line item. It is a compounding force working against you every single year. Every dollar that leaves your account as an advisory fee is a dollar that never compounds. It does not just cost you that dollar. It costs you every dollar that dollar would have become over the next 10, 20, or 30 years. The drag is invisible on your monthly statement but enormous over a lifetime.

The fund manager's incentives make this worse, not better. Your fund manager is evaluated on short-term performance, not long-term outcomes. That means he is not waiting patiently for the right businesses at the right prices. He is buying something with your money right away, because sitting in cash for two or three years, even if that is the smartest move, is not good for his career. His job security depends on looking busy. Yours depends on actually growing wealth. Those are not the same goal.

Only 4% of mutual fund managers consistently beat the market over a 15-year period. The other 96% underperform a basic index fund, and yet they collect their fee every year regardless. You are paying for active management and receiving below-average results in the overwhelming majority of cases.

When investing with a financial advisor, that fee drag is the cost of outsourcing a skill you can learn yourself. Learning to evaluate and buy businesses yourself eliminates it entirely. The fee stops. The compounding starts working in your direction instead of against it.

Why the Financial Advisor System Was Built for Wall Street, Not You

Here is something worth understanding about the 401(k) specifically. I am not a fan of them, and the reason is straightforward: they are built on the assumption that you are incapable of making your own investing decisions. So they hand your money to fund managers and restrict your choices to a limited menu of funds, most of which carry their own embedded fees on top of whatever your advisor charges. You are paying twice, with limited control over either layer.

The system was not designed with your retirement as the priority. It was designed around the people collecting fees from it. Taking control of your own investments is the only way to guarantee that your interests come first.

The S&P 500 Beats Most Financial Advisors

If a financial advisor isn't going to beat the market, why not just invest directly in the market yourself?

The Power of Investing in the S&P 500

The S&P 500 index (which tracks the 500 largest U.S. companies) outperforms most financial advisors over time.

Example: Financial Advisor vs. S&P 500

Let's compare investing $100,000 with a financial advisor vs. putting it into an S&P 500 ETF (like SPY or VOO).

Over 20 years, the investor who simply bought and held an S&P 500 ETF ended up with $115,000 more than the investor paying for financial advice.

Why Do Financial Advisors Underperform?

Diversification Dilution: Advisors spread your money across too many assets, reducing potential gains and complicating asset location strategies.

Regulatory Restrictions: Advisors are limited in what they can recommend, which can impact tax loss harvesting and insurance planning.

Fees Drag Down Returns: Even if an advisor keeps up with the market, their fees reduce your net returns.

If you want to build wealth efficiently, investing in the S&P 500 is a simple, low-cost strategy that beats most financial advisors. It allows you to feel confident about your financial future through more control over your finances and assets.

How to Pick Rule #1 Stocks — Download

Choosing Individual Stocks Can Lead to Even Higher Returns

While investing in the S&P 500 is a great strategy, some of the world's most successful investors, like Warren Buffett, Peter Lynch, and Charlie Munger, have built their fortunes by picking individual stocks and understanding their own risk tolerance.

How to Invest Like Buffett (Without an Advisor)

Unlike financial advisors, individual investors are not restricted by SEC regulations. This means you can:

Identify undervalued companies with strong long-term potential.

Buy stocks when they are discounted due to temporary market fluctuations or turbulent times.

Hold your investments for years or decades to maximize growth even until retirement.

This value investing strategy has created more millionaires and billionaires than any other investing approach. However, it's important to avoid the mistake of emotional decision-making or chasing trends without research.

Real-World Example: Apple (AAPL)

Imagine you invested $10,000 in Apple stock in 2005 instead of paying a financial advisor.

In 2005, Apple traded at around $2.50 per share (adjusted for splits).

By 2024, Apple is trading at over $180 per share.

Your $10,000 investment would be worth over $720,000 today.

Would a financial advisor have recommended Apple? Probably not, because they are often restricted from concentrating investments in high-growth companies.

This is why managing your own investments can be so much more rewarding. It can help you manage your portfolio with a strategy that fits your goals for life and retirement.

Can You Manage Your Own Investments Without a Financial Advisor?

The most common question I hear is some version of this: what if I do it wrong and lose everything?

That fear is worth addressing directly. It is exactly what keeps most people from taking control of their own money.

Rule #1 Is Built Around That Fear

The entire methodology starts with one principle: Don't Lose Money. You do not buy a business unless the price gives you a significant buffer against being wrong. That buffer is called a Margin of Safety, and it means that even if your analysis is partly off, you are still protected because you bought well below what the business is worth. The methodology itself is the risk management.

It Started With $1,000 and a River Guide

I started as a Grand Canyon river guide earning $4,000 a year. No finance background. No investment accounts. A mentor sat me down and walked me through a repeatable system for evaluating businesses and buying them at attractive prices. I started with $1,000 and turned it into over $1 million in five years.

As I have said many times since: "If I can do it with just $1,000, then so can everyone else."

From Skeptic to Confident Investor

My daughter Danielle is a Wellesley, Oxford, and NYU Law-educated attorney. For years she wanted nothing to do with investing. She thought it was too complicated, too risky, not for someone like her.

She spent time learning the Rule #1 methodology from scratch and documented the entire journey in her book Invested. [Publishing team: verify timeframe of Danielle's learning journey before publishing.] By the end of that process she was investing with confidence.

If it worked for a river guide with no investing experience and a lawyer who resisted it for years, it can work for you. Start with our beginner's guide to investing if you want a clear foundation before your first investment decision.

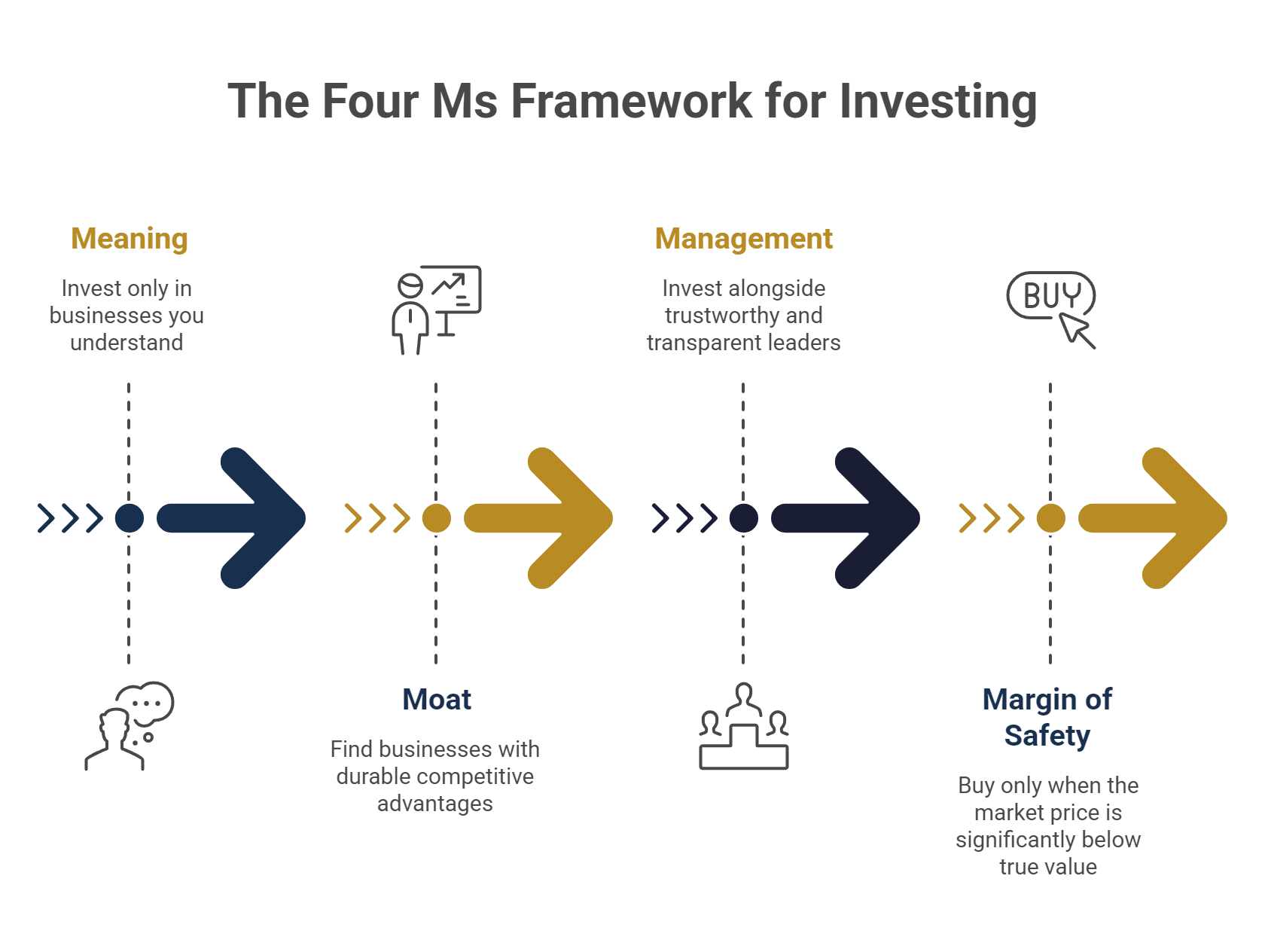

The Four Ms: A Proven Framework That Replaces What Advisors Do

So what exactly does a financial advisor do for you that you cannot learn to do yourself? At the core, it comes down to two things: figuring out which businesses are worth owning, and deciding when the price is right to buy. The Four Ms framework does both, in a structured, repeatable way.

Meaning: Only Invest in What You Understand

The first filter is simple. If you cannot explain what a company does, who its customers are, and why people keep coming back, you have no business owning it. Meaning is not just philosophical. Understanding a business is what allows you to make a rational judgment about its future. If you cannot predict the future of a business with reasonable confidence, you do not buy it. That alone eliminates a large category of speculative mistakes.

Moat: Find Businesses That Can Protect Their Profits

A moat is a durable competitive advantage. It is what protects a company from competitors who want a piece of its market. A brand so strong customers will not settle for a substitute. A patent protecting a formula. A switching cost that makes leaving painful. A price advantage no competitor can match. A business without a moat is fighting on price, and that is not where you want your money.

Management: Invest Alongside People You Can Trust

The people running the business matter. I look for leaders who are owner-oriented, transparent with shareholders, and focused on long-term value rather than short-term optics. The CEO's annual letter tells you more than the quarterly report. If a leader is not being straight with owners about what is working and what is not, that is enough reason to pass.

Margin of Safety: Only Buy at the Right Price

This is where the math comes in. You calculate the true value of the business, what I call the Sticker Price, and you only buy when the market price is significantly below that value. I will not buy without a Margin of Safety. If a genius like Buffett insists on it, so should we. Buying at a deep discount protects you when your analysis is slightly off and accelerates your return when it is right.

This is the system. Four filters applied in sequence. Each one removes a specific category of risk. Used together, they give you a concrete, rational basis for every investment decision you make, without paying anyone 1% of your portfolio annually to do it for you.

Use the Margin of Safety calculator to find your entry point, and explore the full Rule #1 Toolbox to run your complete analysis in one place.

Do I Need a Financial Advisor for Retirement?

The retirement context feels different to most people. The stakes feel higher. And the 401(k) system is genuinely more complicated than a regular brokerage account. So let me address it directly.

You Have More Control Than You Think

Even within a limited 401(k) fund menu, the Four Ms way of thinking helps you make better choices.

Ask yourself:

Which fund has the lowest expense ratio?

Which actively managed option has consistently outperformed its benchmark over 10 years, not just 3?

Which allocation makes sense given where you are in your career?

These are questions you can answer yourself once you understand how to evaluate value and cost.

The Self-Directed IRA Option

If your 401(k) restrictions feel truly limiting, look into rolling it over into a self-directed IRA. Every major online broker can walk you through that process without any tax penalty. A self-directed account gives you the freedom to buy individual businesses, not just whatever funds your employer's plan administrator selected for you.

Run Your Own Numbers First

Before deciding whether you need professional help with retirement planning, see where you actually stand. Use our free Retirement Calculator to see exactly what rate of return you need to reach your goals and how different fee levels affect that outcome over time.

For a deeper look at how the fee structure inside most retirement accounts works, read our guide on 401(k) plans and mutual fund investing.

Should You Ditch Your Financial Advisor?

Financial advisors have their place, especially if you need expert guidance on estate planning, tax strategies, or retirement planning, or if you want a sounding board to help you avoid emotional investment decisions.

But for long-term wealth building specifically, you do not need one. The tools, the framework, and the education are available to you. The Virtual Investing Workshop is where most people take that first practical step.

By taking control of your investments, you eliminate unnecessary fees, gain full transparency over your money, and put yourself in a position to outperform most financial advisors. This approach empowers you to manage your finances for your business, your family, and your future.

You can also follow our step-by-step process to get started at your own pace.

Final Thoughts: Take Charge of Your Financial Future

If you are still asking yourself 'should I get a financial advisor,' here is my honest take: they are not bad, but for most people, they are not necessary.

The knowledge, the tools, and the framework to manage your own investments are all available to you. My goal has always been to teach people how to take control of their finances so they do not have to pay someone else who will get them a mediocre return at best. That has not changed.

Key Takeaways

Financial advisors focus on coaching, not beating the market.

Their fees compound against your wealth every year, regardless of performance.

The S&P 500 outperforms most financial advisors over time.

Investing in individual companies you understand can yield even greater results.

Managing your own investments eliminates unnecessary fees and puts you in full control.

If you are ready to learn how to do this yourself, we do not just talk at you. You practice in real time with live Rule #1 mentors. Show up ready to learn and I will make sure you know what you are doing.

Phil Town

Phil Town is an investment advisor, hedge fund manager, 3x NY Times Best-Selling Author, ex-Grand Canyon river guide, and former Lieutenant in the US Army Special Forces.